Affordable Housing Is Harder to Build Than We Want to Admit

Affordable housing isn't manifested into being by slogans, yard signs, or mandates. It gets built when the math works. A look at the development pro forma behind a modest four-unit project — the financing gap it revealed, the capital stack that closes it, and what Ann Arbor already gets right.

A comment I see often in local housing conversations goes something like this: “Less luxury, more affordable housing needed.”

I understand the sentiment. Ann Arbor needs more housing, and we especially need more housing that working people, young families, seniors, students, and lower-income residents can actually afford. But every time I see a comment like this, I want to ask one more question:

Who is going to build the affordable housing?

That is not a cynical question. It is the practical question underneath the moral claim.

Because “more affordable housing” is easy to say and very hard to build. I know this from sitting through public meetings, reading local housing debates, lurking and occasionally posting on Nextdoor and Facebook, and watching people tune out the moment the conversation moves from values to financing. That is why I am writing this.

At the Building Michigan Communities Conference, I attended a track for elected and appointed leaders where we worked through a basic housing development pro forma. In plain English, we looked at the math behind building housing. Not luxury towers. Not massive apartment complexes. Just a modest four-unit project in a traditional single-family neighborhood — the kind of neighborhood that, by zoning, has long allowed nothing but detached single-family homes: two market-rate homes and two affordable homes. And even there, the math was sobering. The lesson I walked away with was simple:

Affordable housing does not happen just because we demand it. Someone has to close the financial gap.

I went into the session already believing that Ann Arbor needs more housing, including more deeply affordable housing. I still believe that. Strongly. But I left with a clearer understanding of something I think we often skip over in public conversations: affordable housing is not created by moral clarity alone. It is not built because we want it badly enough. It is not "manifested" into existence through slogans, yard signs, or even relentless public comment. Affordable housing gets built when the math actually works. And right now, the math is very hard.

The exercise that changed how I think about the problem

As part of the track, our presenter walked us through a development pro forma. A pro forma is basically a financial worksheet that helps a developer, lender, investor, or public official understand whether a project can actually be built.

The project we worked through was modest. This was not a luxury high-rise. It was not a massive apartment building. It was a small four-unit development in a traditional, exclusionary, single-family-only neighborhood. Two of the units were market-rate. Two were affordable.

That is the kind of project many of us say we want: gentle density, mixed income, small scale, more housing choice, and some affordability built in. But even in that relatively modest scenario, the numbers were sobering.

The bank was not going to finance the whole thing. That makes sense. Banks are not philanthropic institutions. They lend based on risk, projected income, collateral, and their own underwriting standards.

One of the key concepts in the exercise was the Debt Service Coverage Ratio (DSCR). In simple terms, banks want to see that a project's income will comfortably cover its loan payments — typically by a margin of roughly 1.15 to 1.20. If the projected rents are not high enough to support a larger loan, the bank simply won't lend more, regardless of what the project costs to build.

In our exercise, that underwriting limit meant the primary lender would finance only about 48% of the development cost. The remaining 52% had to come from somewhere else and that gap was not small. It needed to be filled by some kind of secondary source: investor capital, limited partners, public subsidy, tax increment financing, a community bank, a brownfield incentive, local affordable housing funds, or some other layer in the

capital stack.

Want to Try the Math Yourself?

One of the reasons housing debates can become frustrating is that most of us never see the financial assumptions behind a project. To help make the conversation more concrete, I've recreated a simplified version of the housing development pro forma we used at the Building Michigan Communities Conference.

You can experiment with construction costs, rents, financing assumptions, affordability requirements, and other variables to see how quickly funding gaps emerge—and what it takes to close them.

You may come away with different policy conclusions than I do, but I suspect you'll leave with a deeper appreciation for just how difficult affordable housing can be to finance and build.

That was the moment the abstract became concrete for me.

We talk about “requiring affordable housing” as if the requirement itself creates the money. It does not. A requirement creates an obligation. It does not automatically create the financing needed to meet that obligation.

Someone has to close the gap

Sometimes the answer is the state or federal government through tools like the Low-Income Housing Tax Credit program. LIHTC was created through the 1986 federal Tax Reform Act and is now one of the primary tools for financing affordable rental housing in the United States. In Michigan, it is administered by the Michigan State Housing Development Authority, or MSHDA.

But however we do it, the gap has to be closed. There is no magic wand. There is only a capital stack.

What Ann Arbor gets right

This is one reason I appreciate some of the tools Ann Arbor has already created. We have an affordable housing millage. That matters. It creates a dedicated local revenue stream for affordable housing.

We also have an affordable housing trust fund. That matters too. In some cases, market-rate development contributes to that fund, especially when developers seek additional value through zoning or density. That money can then help support affordable housing elsewhere.

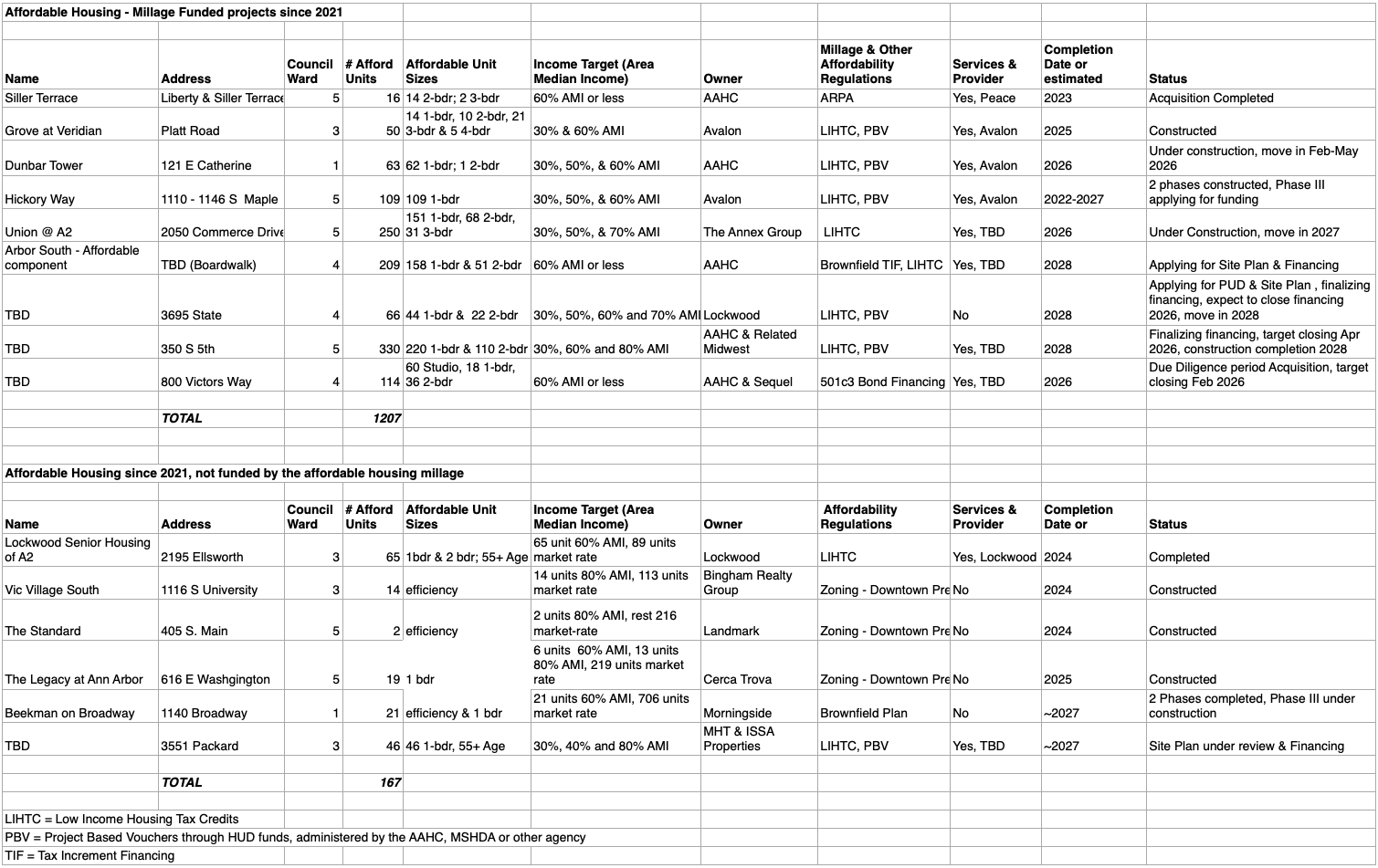

These tools are not perfect. They do not solve everything, and they do not produce affordable housing at the scale we need. But they are real. Since 2021, Ann Arbor has roughly 1,207 affordable units completed or in the development pipeline with help from the housing millage and another 167 built or underway without millage funding, through zoning incentives, brownfield plans, and tax credits. That is more than 1,300 homes.

And if you look at how they were financed, almost none of them rely on a single source. They weave together tax credits, project-based vouchers, brownfield incentives, bond financing, and local millage dollars. That weave is the capital stack. These units are not abstractions nor just policy victories. They are real homes for real people.

Housing is a justice issue. Exclusionary zoning has done real harm. Single-family-only neighborhoods have often functioned as tools of racial and economic exclusion. The lack of affordable housing in Ann Arbor is not an accident. It is the result of decades of policy choices, market dynamics, scarcity, and political resistance. In some cases, it reflects the deliberate efforts of neighbors who have spent almost 100 years trying to prevent change.

So yes, we need urgency. Yes, we need imagination. Yes, we need public courage. But we also need financial literacy. We need to know the difference between a slogan and a subsidy, between a mandate and a funding source, and between what we wish were true and what the numbers say is possible. And then we need to change what is possible.

I believe in prophetic imagination. I believe communities can become more just than they are. I believe public policy can bend toward the common good. I believe we can build a city where more people can belong.

But prophetic imagination is not the same thing as pretending.

We cannot simply declare that affordable housing should exist and then act surprised when it does not get built. We cannot manifest it into being. We have to finance it, zone for it, subsidize it, make land available for it, and welcome the neighbors who will live in it.

That is the lesson I took away from the conference. Affordable housing is difficult to build. Not impossible. Difficult. And because it is difficult, the financing side cannot be treated as an afterthought. It is central to the conversation.

If we want affordable housing, we have to answer the question that sits underneath every public debate: Who is going to close the gap?

Because the gap will not close itself.